You love West Austin for its views, lakes, and Hill Country lifestyle. But the same terrain that makes it special can also amplify wildfire and flash‑flood risk. If you are buying or selling in western Travis County, understanding these hazards can protect your plans and your investment. This guide gives you clear steps, local tools, and what to watch in permits, maps, and insurance so you can move forward with confidence. Let’s dive in.

Why risk looks different in West Austin

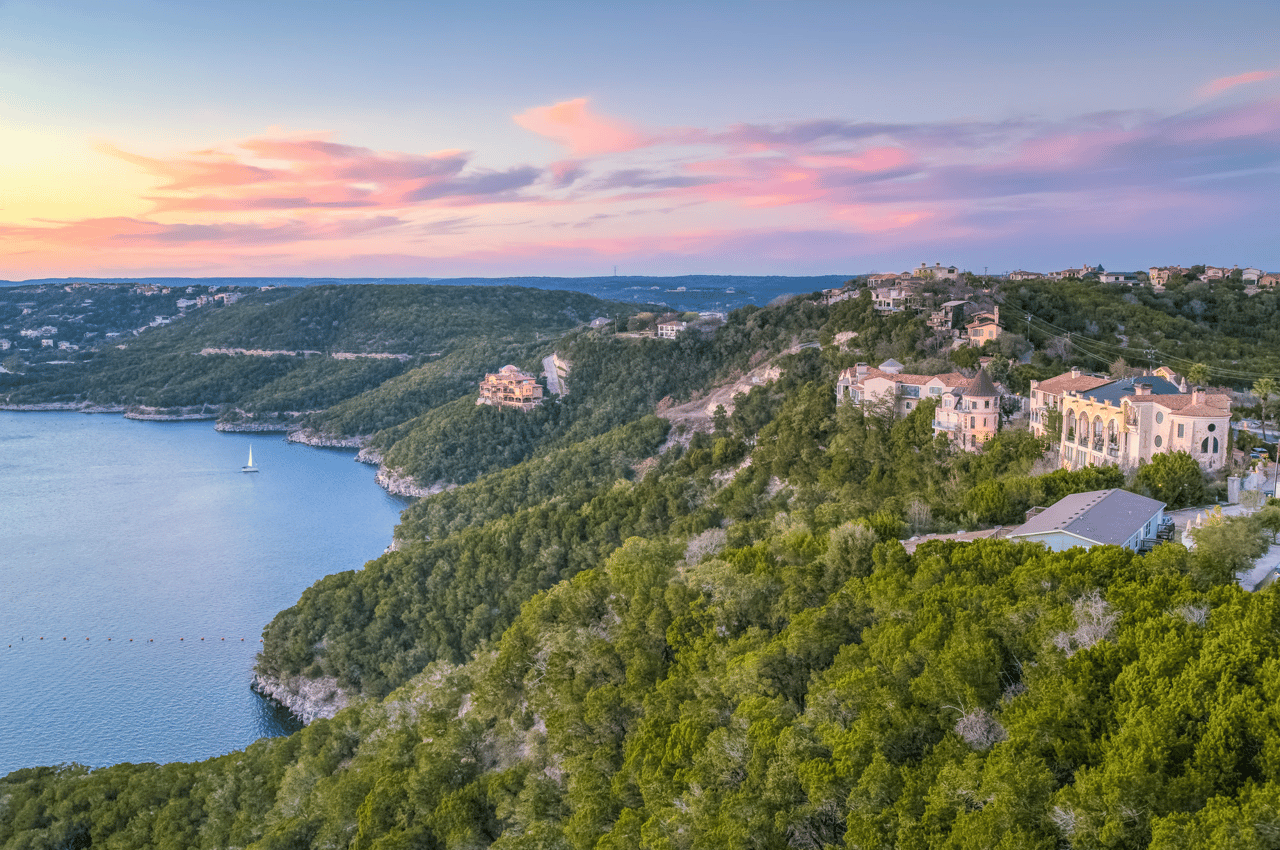

Steep slopes, shallow rocky soils, and narrow creek channels define the Texas Hill Country. Those features speed runoff during heavy storms and create wildfire‑prone edges where neighborhoods meet native vegetation. Recent Hill Country floods and fires show how quickly conditions can change and why site‑specific due diligence matters. The Texas Tribune’s reporting on Hill Country floods highlights the region’s flash‑flood history and evolving risks.

Austin is also updating how it plans for storm rainfall. NOAA’s Atlas 14 shows higher rainfall totals for rare events, which drives larger mapped floodplains and stricter rules until remapping is complete.

Flood risk in the Hill Country

How flash floods happen here

Hill Country floods are often fast. Steep hills plus thin soils push rainwater into creeks in hours. That puts low‑water crossings, riverfront parcels, and canyon bottoms at higher risk during intense storms.

Read the right flood maps

- FEMA Flood Insurance Rate Maps outline Special Flood Hazard Areas, which most lenders use for insurance requirements. Learn how those maps work on FEMA’s floodplain management page.

- Inside the City of Austin, use the property‑level FloodPro tool to see current regulatory status while the city updates maps for Atlas 14.

- FEMA has also issued revised maps for parts of Travis County. See the update process in FEMA’s Travis County map notice.

Insurance basics and common gaps

Standard homeowner policies usually exclude flood. NFIP and private policies cover this peril. Lenders require flood insurance for homes in FEMA‑mapped high‑risk zones, but flood damage can and does occur outside them. Review the basics on FEMA’s flood insurance page.

Flood due diligence checklist

- Look up the address in FloodPro (if within Austin) and compare with FEMA maps.

- Request the TREC Seller’s Disclosure and any prior elevation certificates.

- If near a mapped floodplain, consider ordering a new elevation certificate.

- Get NFIP and private flood insurance quotes early so costs do not surprise you.

You can access the Seller’s Disclosure form on TREC’s website.

Wildfire risk in West Austin

Why the WUI matters

Many West Austin neighborhoods sit in the wildland‑urban interface, where homes meet oak‑juniper and grass fuels. Embers and radiant heat are the leading ways homes ignite during a wildfire. The takeaway is simple: focus on how your home is built and how the first 100 feet around it are maintained.

Regional risk snapshot

Austin is among the U.S. metros with a large number of homes at moderate or greater wildfire risk, according to the CoreLogic 2024 Wildfire Risk Report. That context helps explain recent code updates and mapping.

Austin’s WUI Code and map

Austin adopted an updated Wildland‑Urban Interface Code with a WUI zone map that guides building materials, defensible‑space, and permit requirements for new construction and major remodels. Before you buy or plan a renovation, check a parcel’s zone on the city’s WUI Code page.

Home hardening and defensible space

- Roof: Class A where required. Keep gutters clean.

- Vents: Use ember‑resistant covers and seal gaps.

- Decks and fencing: Favor noncombustible or ignition‑resistant materials.

- Vegetation: Create an “Immediate Zone” 0–5 feet that is clear of combustibles, thin and limb up within 5–30 feet, and manage fuels 30–100 feet out.

For a concise checklist, see the U.S. Forest Service guide to making your home wildfire defensible.

Grants and local help

Cost‑share programs can offset mitigation work like fuel reduction. Explore Texas A&M Forest Service opportunities on the Fire Mitigation Grants page.

Where flood and wildfire risks overlap

Some Hill Country parcels face one or both hazards. Creek‑adjacent and low‑lying lots see higher flood exposure. Ridgeline and wildland‑edge sites can see more ember exposure during fire weather. As you compare homes, weigh which hazard could create the larger financial loss and which mitigation steps are feasible at that address. This Hill Country overview explains how terrain drives these tradeoffs.

A fast decision framework

- Waterfront or creekside: prioritize flood elevations, access during storms, and insurance.

- Hillside or ridgeline: prioritize defensible space, construction details, and access for responders.

- Steep canyon above a creek: plan for both hazards and budget for mitigation work.

Seller notes and required disclosures

Texas requires the Seller’s Disclosure Notice to address flooding history, flood insurance, and whether a property lies in a 100‑ or 500‑year floodplain. Make sure buyers receive the completed form and verify answers with maps, elevation documents, and insurance quotes. Review the current form on TREC’s site.

Next steps for confident decisions

- Start with FloodPro, FEMA maps, and the Austin WUI map before you fall in love with a view.

- Price in the cost of insurance and any mitigation work alongside your renovation plans.

- Use disclosures, elevation data, and property‑specific inspections to confirm what maps suggest.

If you want a calm, private path through this due diligence, connect with Megan DiBartolo to align the right Hill Country home with your long‑term goals.

FAQs

How do I tell if a West Austin property is in a flood zone?

- Check the address in Austin’s FloodPro and compare to FEMA’s Flood Insurance Rate Maps, then confirm with an elevation certificate if the home is close to a mapped floodplain.

Do I need flood insurance if my lender does not require it?

- It is often wise to consider it because flood damage can occur outside mapped high‑risk zones; confirm costs and coverage early using NFIP and private quotes.

Are hilltop homes safer from floods but more exposed to wildfire?

- Generally yes; higher ground lowers inundation risk, but ridgelines and wildland edges can face more embers and heat during a wildfire, so home hardening and defensible space are key.

Could Austin’s WUI Code or flood rules affect my renovation?

- Yes; if the parcel lies in a WUI zone or mapped floodplain, certain materials, clearances, and elevation or permit conditions may apply to new construction and substantial remodels.